Sustainability - no time to waste Insurers’ role to make the world be sustainable

by Mi Young Kim, Manager, Kyobo Life Insurance Co., Ltd.

Sustainability-No time to waste

In Feb. 2021, Samsung Electronics had to shut down its semi-conductor plant in Austin, Texas, due to severe snowstorm in the region. How did the snowstorm affect the chip plant? The storm brought days of subfreezing and widespread power outages and the company was the largest consumer of the power of Austin. As millions of Texas homes and businesses lost electricity and the state’s power grid came close to a total shut down, the energy officers of Texas ordered the company to shut down its plant.

Samsung Electronics lost over $270Million from the shut down of its operation which continued for more than a month and hundreds of deaths was witnessed in Austin.

Scientists said a warming earth could bring extreme weather events as rising temperature disrupting polar vortex. They suggested that the cold snap in Texas, which was the coldest February in more than four decades, was also caused by climate change.

Climate change is not a word which simply addresses increase in the earth’s temperature. Associated consequences need to be considered together and in such context climate change means that the living condition and business environments will no longer be predictable and controllable.

Why ESG Matters in Insurance?

So, how is climate change associated with the insurance industry? Insurance companies are not like manufacturers who generate pollution.

I believe for insurance companies (like other companies) sustainability is an important consideration to meet the ‘going concern assumption’ as an enterprise, for reasons amongst others ESG (Environmental, Social, Governance) issues would affect profit of insurance companies.

Recent report from Swiss Re[1] stated that ‘the health and mortality impacts of climate change to play out gradually with incremental impact on life and health risks, although a potential for shock events such as pandemics remains’. The main idea of the report was climate change which led to extreme heat, air pollution, and increased exposure to infectious disease spread by non-human vectors. Consequently, increased morbidity of non-communicable diseases, and increased spread and emergence of tropical infectious diseases, is expected. Therefore, ultimately, climate change could push the mortality/ morbidity rate higher.

No insurance company have taken into account the climate risks into their underwriting risks until now. That means the climate change could erode mortality/morbidity gain of insurers, which is a long term and stable profit source for insurance companies.

“What is Insurance? It is risk management!

The role of insurance company is risk management, and its profit also comes from risk management.

What are we contributing to climate risk management? Where is our role? We need to carve out our niche for contribution to prevention rather than be passive about managing the outcome of the occurrence of risk. We need to prevent it!

Recommended Policy Action for Insurance Companies

When we look back at history, every revolution has been triggered and completed by individuals. At the same time, we witnessed that the capital market had power to alter investors’ behavior.

Insurers have unique features –i.e., insurers have been connected to both individuals and capital markets for a long time. Therefore, I believe insurers can play an important role in making the earth sustainable.

Product

More customer benefits for more ESG activities.

In general, the number of clients of a major insurance company is over millions. For example, the number of policy holders of Kyobo and Samsung Life in Korea is over 12 million, which amounts to a quarter of the total population of South Korea. Therefore, if an insurer provides product encouraging its policyholders to E(Environmental) or S(Social) activities, it will have an impact on millions of individuals. To give a specific example, if an insurer designs a product that provide premium discount – just like what we do for long-term prime customers – when a policy holder achieves missions like using public transportation, reducing electric consumption, or making donations. More ESG activities led to more discount. We can make this procedure like mission clear game, providing target and mission map through mobile, adding ‘fun factors’. Thanks to the evolving technology, insurer can verify or gather the above data utilizing ‘Scrapping’ technology, enables a company using certain data stored in other company’s data base with a consent from the individual who provided the data. If an insurer has the technology, it can not only easily gather ESG related data from a credit card company, a utility company, or a charity but also readily incorporate the data into insurance premium.

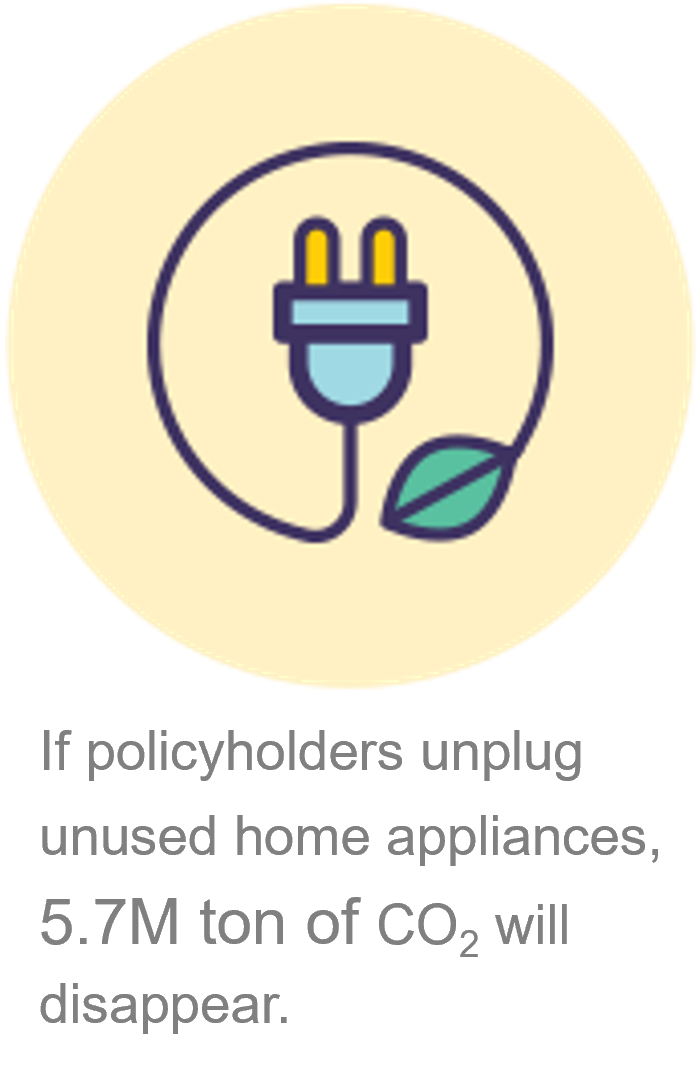

Considering long-term nature of life insurance products, the ESG features of a policy is persistent. When we think about the multiplied impact - large client pool of insurance companies and the long contract period of a product, the impact of those products deserves strong attention. Let me take a mission ‘using public transportation’ as an example. If a person uses public transportation instead of driving a car once a week, it will reduce 469.4kg of carbon dioxide per year, same impact as planting 71.1 trees. Also, if a policyholder unplugs home appliances when they are not used, carbon dioxide emission declined by 12.6kg per year. When we assume all policyholders of Kyobo Life and Samsung Life use public transportation once a week and pull off the plug on their home electronics, 5.7million ton of CO2 emission will disappear. This emission reduction is 23% of target NDC[2] that Government of Republic of Korea submitted to UN. Please remember, I have assumed participation of only two major insurance company’ policyholders in just two simple activities.

Organization

Creating virtuous circle for Sustainability.

As of end of 2022, the number of employees of life insurance companies was 22,836. If we include the number of financial planners, the number climbed to 101,728[3].

Insurers should nudge their employees to protect environment and serve social values by providing relevant infrastructure. To elaborate in detail, a company provides mobile application for its employees for car-pooling. This mobile application marks each employee’s home address on the map, so that an employee can know who lives in the neighborhood. The neighborhood employees chat with the car owner and make an appointment to meet. Also, the application shows where the car is using the GPS of car owner’s mobile phone. If four people share one car, the carbon emission will be reduced to one quarter.

In addition, a corporation also can link employees’ benefit to ESG activities. For instance, it is possible to calculate each team’s electronic or water consumption, and amount of waste produced. Every month, corporation announces the team that has best contributed to reduce carbon foot prints and grant cafeteria card points to the members of that team. The granted points can be used to donate for the underprivileged, to buy eco-friendly products, or to invest in ESG projects such as construction of green building. This whole procedure makes virtuous circle for sustainability by expanding one ESG activity (i.e. reducing carbon dioxide emission) into another (i.e. supporting the underprivileged). This is also economically beneficial to the company in that it can cut indirect expenses such as supplies expenses, electricity bill, or water bill. If every employee working in the insurance industry uses computer energy saving program and green touch, greenhouse gas can be reduced by 1.8 million ton per year. If 100,000 employees make donation to Unicef by using the benefit points of U$25, 1.8 million children in East Africa can be provided with sufficient nutrients for a month. If all people engaged in the insurance industry around world participate in the movement, we can save all children suffering from hunger and disease.

Enhancement of Gender Parity.

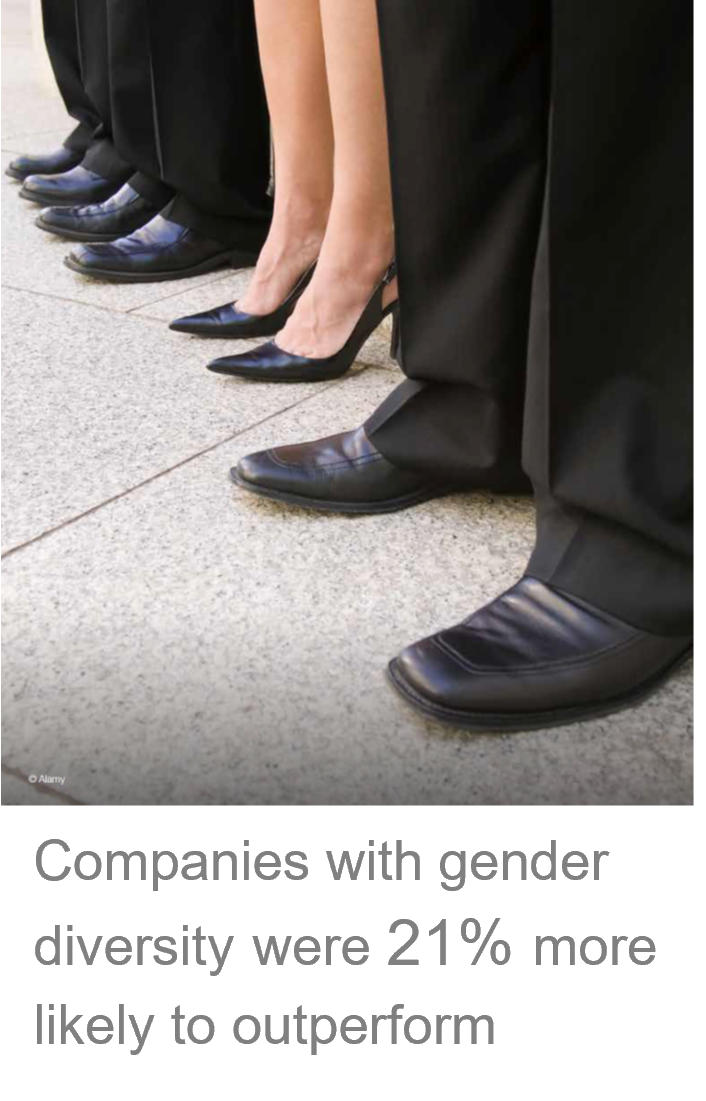

An insurance company should immediately improve gender equity by providing flex time system to employees. According to the book named career and family written by Claudia Goldin, the salary gap between female and male starts from child birth, because mom workers usually take care of their children, not being able to respond 24 hours of on call from their job. If a company operates flex time system – a system that employees can choose working hours and how much time they work per week - mom workers can take care of their children without career break and work enough time to achieve their career goal. All that the insurer has to do is just tally up the total working hour. The system will lead to longer years of service for woman as well as higher performance of female employees. As a consequence, the disparities in salary and promotion will be narrowed. IMF analysis suggest that if Korea’s female labour force participation rose to the same level as male labour force participation by 2035, real GDP would grow by more than 7 percent. Improving gender parity is also beneficial for a company. A company can fully utilize 50% of work force in the world attracting larger talent pool, and retain qualified female employees. They will be loyal to the company that cares for their family and life, too. Without or with very little cost, a company can secure talented employees. A study by Mckinsey and Co. Management Consultant[4] found that “companies in the top quartile for gender diversity on executive teams were 21% more likely to outperform on profitability.” In addition, Swiss Re[5] institute estimates that a 26% increase in global GDP in a scenario of labour market gender parity would yield an additional U$ 2.1 trillion in global insurance premiums by 2029. It also models that gender equity would reduce existing health protection gaps in Asia by 11%.

Investment

Expansion of ESG investment.

As of 2022, total operating assets of Korean life insurers marked U$ 577 billion. Currently, less than ten percent of assets of insurance companies are allocated in ESG projects. As their liability duration is long, life insurers prefer long-term investment to manage asset-liability duration gap. In other words, life insurers have capability to invest huge amount for a long investment horizon. These features of asset management are exactly suitable for investing in ESG projects. Let me take renewable energy plant construction project as an example. To build a power plant, though it would depend on each project, approximately U$ 400 million of cash is required to be injected. Most of renewable energy power plant projects are supported by the government, resulting in stable cash flow and profit. The life span of infrastructure typically lasts several decades. Long term, constant and stable cash flows - the conditions that insurers are fond of are all included in ESG projects. Also, unlike global asset management firms, insurers are not sensitive to short-term return. That brings strong comparative advantage to insurers when they intend to stick to the long-term target.

Investment in ESG projects creates significant impact given the large capital size. For instance, Kyobo Life invested its ESG bond proceeds of U$ 400 million in renewable energy projects, clean transportation, and affordable housing projects. The investment reduced 96, 611 ton of carbon emission, improved accessibility of 14 million people, supported 140 million Korean won to the poor. Only one bond’s proceeds have made such differences. This is the power of insurance company.

From the perspective of capital management, issuing ESG bond led to less funding cost. Investment bankers said that issuing ESG bond is definitely beneficial to issuers - though they cannot measure how much spread would be tightened compared to non-ESG bonds - because the ESG feature contributes to creating momentum on the course of book building process, given the fact that major investors is operating ESG dedicated funds.

Be the Company that Generates Sustainable Profit

To conclude, I do not suggest to ‘be a socially responsible company’. What I suggest is to ‘be a company that generates sustainable profit’, which meets concept of ‘going concern’ assumption of an enterprise. Especially, an insurance company is an optimized organization to pursue sustainability for reasons I presented above.

- Insurance companies have been connected to individuals and capital markets for decades and will continue to do so.

- Insurance companies have massive client pool and operating assets. As a result, their ESG strategy has the capability to affect the global society.

Utilizing those strengths, insurers can enjoy continuous and stable profit across the generation pursuing sustainability. Hence, I suggest, we, insurers, become a game maker in ESG universe.

[1] The risk of a life time: mapping the impact of climate change on life and health risks, Jan. 2023 by Swiss RE Institute

[2] NDC: Nationally Determined Contribution

[3] Source: Korea Life Insurance Association

[4] Power of Parity: How advancing women’s equality can add $12 trillion to global growth, September 1, 2015 by Mckinsey global institute

[5] Why gender equality matters for insurance, August 2019 by Swiss RE Institute