Insurers Can Innovate with Purpose to Change the World (Again)

Click here to read Chunk Mui's bio

View More Articles Like This >

IIS Executive Insights Innovation Expert: Chunka Mui, Futurist and Innovation Advisor

Setting innovation aspirations for changing the world might sound hyperbolic in the context of most industries but doing so is deep in the history and DNA of insurance. The innovations centered at Lloyd’s Coffee Shop on the docks of late 17th century London didn’t just sell more coffee; they enabled a massive expansion in global maritime trade. This, in turn, drove both innovation in shipping and economic development across many other industries and geographies.

This pattern, often repeated, reveals a larger purpose for insurance: to help drive safety, security and development for society at large. History shows that quantifying and spreading risk to protect against loss creates a virtuous cycle for mitigating risk and making the world a better place. At its best, the insurance industry is both catalyst and lubricant for societal innovation.

As Rowan Douglas, head of the Climate and Resilience Hub at Willis Towers Watson, has observed, “It was the insurance sector that made the electric system of the world safe, through the underwriters' laboratories. We have, broadly speaking, safe cars and safe road layouts, because there was an economic agent called the insurance industry which demanded those things.”

It is time for the insurance industry to do it again. Systemic, purpose-driven innovation would add credibility to the environmental, social and governance (ESG) strategy with which every insurer CEO and Board is wrestling. It would address talent, brand and trust challenges. And, most importantly, it would make a huge difference for society at large.

In this article, I will explore two massive gaps—risk protection and technology—that reveal both the need and the tools for world-changing innovation. In my next article, I offer five strategies to help every insurer uncover big, bold innovation options to pursue.

Gap 1: The Risk Protection Gap

A few years ago, a corporate risk manager stood up in front of an International Insurance Society (IIS) global gathering of industry executives to offer a withering criticism. The executive was responsible for managing a broad range of enterprise risk. However, the insurance products available to him covered only about a third of those risks.

Covid-19 has dramatically spotlighted some of these uncovered risks. According to APCIA estimates, for example, US small businesses of less than 100 employees, are suffering $255 to $431 billion in monthly costs as a result of business closures and related economic slowdown. That, of course, is just a fraction of the damage, and larger, more resilient organizations were not immune. The damage has been widespread and global, hurting economies large and small, rich and poor.

One telling indicator of the level of uninsured losses due to the pandemic is that governments around the globe have already committed more than $10 trillion to address its health, social and economic damage. This price tag (which continues to grow) includes direct spending, equity injections, loans and guarantees. For context, global life and general insurance premiums in 2019 totaled $6.3 trillion, according the Swiss Re. $10 trillion is five times more than what all the countries on the planet collectively spent on military, weapons and war in 2019. It is a staggering 11.9% of pre-COVID global GDP. And, yet, this is not enough. Euler Hermes expects a 31% rise in global business insolvencies in 2021, compared to 2019, as temporary support measures come to an end.

As we know, almost none of this economic devastation was due to physical damage (though this issue is sure to be litigated for a long time). This shines a giant spotlight on the need for corporate risk managers and other insurance buyers to look beyond physical damage triggers to loss. It also highlights the societal need (and therefore the insurance innovation opportunity) for insurers to help customers do so. We are in a “teachable moment” for both policyholders and underwriters to reevaluate what is worth insuring and what is insurable.

Pandemics are far from the only items on this list.

The rapid shift to remote work and redoubled emphasis on the digitization of the insurance value chain prompted by the pandemic is also happening in most other industries, too, and highlights another risk protection gap: cyber risk.

As technology becomes more intertwined with an ever-greater portion of global GDP, that risk will grow in size and complexity. For example, a 2019 study sponsored by Lloyd’s of London estimated that a single large cyber-attack hitting major ports across the Asia-Pacific region could cost as much as $110 billion, just 8% of which are currently covered by insurance.

To put that one potential incident into perspective, there were 820 natural catastrophe events in 2019 worldwide, according to Munich Re. These events totaled $150 billion in losses, of which $52 billion or 35% were insured. It is not surprising then that cyber risks have become the top risk concern for businesses, according to the latest Travelers Risk Index.

Even as cyber and other intangible risks rise in mindshare, the natural catastrophe protection gap (uninsured losses as a share of total losses) remains stark. Munich Re estimates that this gap stands at about 70%, or about 0.2 percent of the world’s GDP. Swiss Re projects the future natural catastrophe protection gap at more than $150 billion per year, or about .25 percent of global GDP. In some developing economies, the natural catastrophe protection gap reaches as high as 95%. But this gap engulfs all economies. Wildfires continue to raze California, and fire insurance coverage will no doubt drop when the current one-year moratorium on policy cancellations expires. We also know there are going to be earthquakes in California, yet 90% of commercial buildings and 80% of homes are not insured for earthquakes.

And, there’s climate change, which Bill Gates recently noted could be worse than the pandemic: “If you want to understand the kind of damage that climate change will inflict, look at COVID-19 and spread the pain out over a much longer period of time,” wrote Gates. “The loss of life and economic misery caused by this pandemic are on par with what will happen regularly.”

Few scientists or underwriters doubt that the number and severity of climate-related events will grow and, left unaddressed, the protection gap will surely grow with it.

The protection gap due to climate change doesn’t just apply to catastrophic events or to developing economies. Take Florida, for example. Once investors and insurers decide that the value of too many 30-year mortgages in that very flat, coastal state face an unacceptable level of risk due to the steady rise of sea levels, many mortgages will go underwater or even be thrown into default due to the lack of mortgage insurance. (Florida’s sea level has risen by eight inches since 1950. The speed of rise has accelerated over the last ten years and is now rising by one inch every three years. Scientists know this because sea levels are measured every six minutes using equipment like satellites, floating buoys off the coast, and tidal gauges to accurately measure the local sea level as it accelerates and changes.)

Even worse for the rest of Florida, as I’ve written, financing for new long-term mortgages, utility debt offerings, and municipal bonds for schools, roads, bridges, sewers, etc., will dry up. That in turn will deflate real estate values overall and crush the backbone of the Florida economy—and send Florida into a deep and costly tailspin. Proactively forestalling such a scenario should squarely be among the world-changing aspirations of insurers who care about, and are invested in, Florida.

To be clear: many risks—like climate disruption, pandemics, sea-level risk, earthquakes and wide scale technology failures—are beyond the strength of insurance industry balance sheets to completely cover. Innovation, however, is not necessarily about covering the entire risk. There are many ripe opportunities for insurers to help governments, which often play the role of insurers of last resort, to better draw the line between public and private insurance and reimagine how this line could change over time. There are also much that could be done to help organizations and individuals, respectively, to create capacity, capability and resilience to better address their risk protection gaps.

The tools to do so can found in each company’s technology gap, and by turning that current liability into a world-changing asset.

Gap 2: The Technology Gap

No company could be competitive in any line of insurance today without some high level of competency in leveraging technology in every aspect of the insurance value chain, including products, underwriting, distribution, claims and customer service. Yet, every insurer faces a substantial gap between the technology available to them and the technology that they are deploying. And, therein lies an enormous opportunity.

The reasons for the technology gap are unavoidable.

First, every company optimizes around the value chain for its current products and services. The more successful a company is at this optimization, the better it does and the more it will continue to systemically leverage technology to get incrementally faster, better and cheaper. This is why there are no lack of “digital transformation” programs on your agenda. This leaves a natural (and economically rational) gap in the application of technology outside of current focus areas.

Second, as anyone familiar with Moore’s Law knows, computing capabilities have been improving exponentially for the last 50 years while simultaneously decreasing in per unit cost—and will continue to do so for the foreseeable future. This is why the smartphone in your pocket has over 100,000 times more processing power and one million times more memory than the computer that guided Apollo 11 to the moon and back —at a percentage of smartphone versus computer cost that effectively rounds to zero. While computing power obviously isn’t free, as anyone buying a smartphone knows, it looks almost free from any historical distance.

Computing power is one of a six key technology-driven resources that follow what Paul Carroll and I have termed the Laws of Zero, meaning that they are headed towards zero cost and therefore infinite amounts can be imagined as available for the future.

Five other Laws of Zero follow the same trend line. We’re seeing communication costs likewise head to zero. Just compare the cost of all those Zoom calls you’ve been on in the last several months to what such calls would have cost 10 years ago. The costs for gathering information will drop steeply, too, as sensors, drones and satellites cover the world. Energy costs are heading to zero(ish) if you look at the stunning drops in price for solar and wind installations and improvements in batteries. If energy becomes free(ish), then so will water—saltwater can be turned into fresh at scale, and water can be condensed out of thin air even in the driest spots on the planet. The costs of transportation will also plunge once driverless cars hit scale.

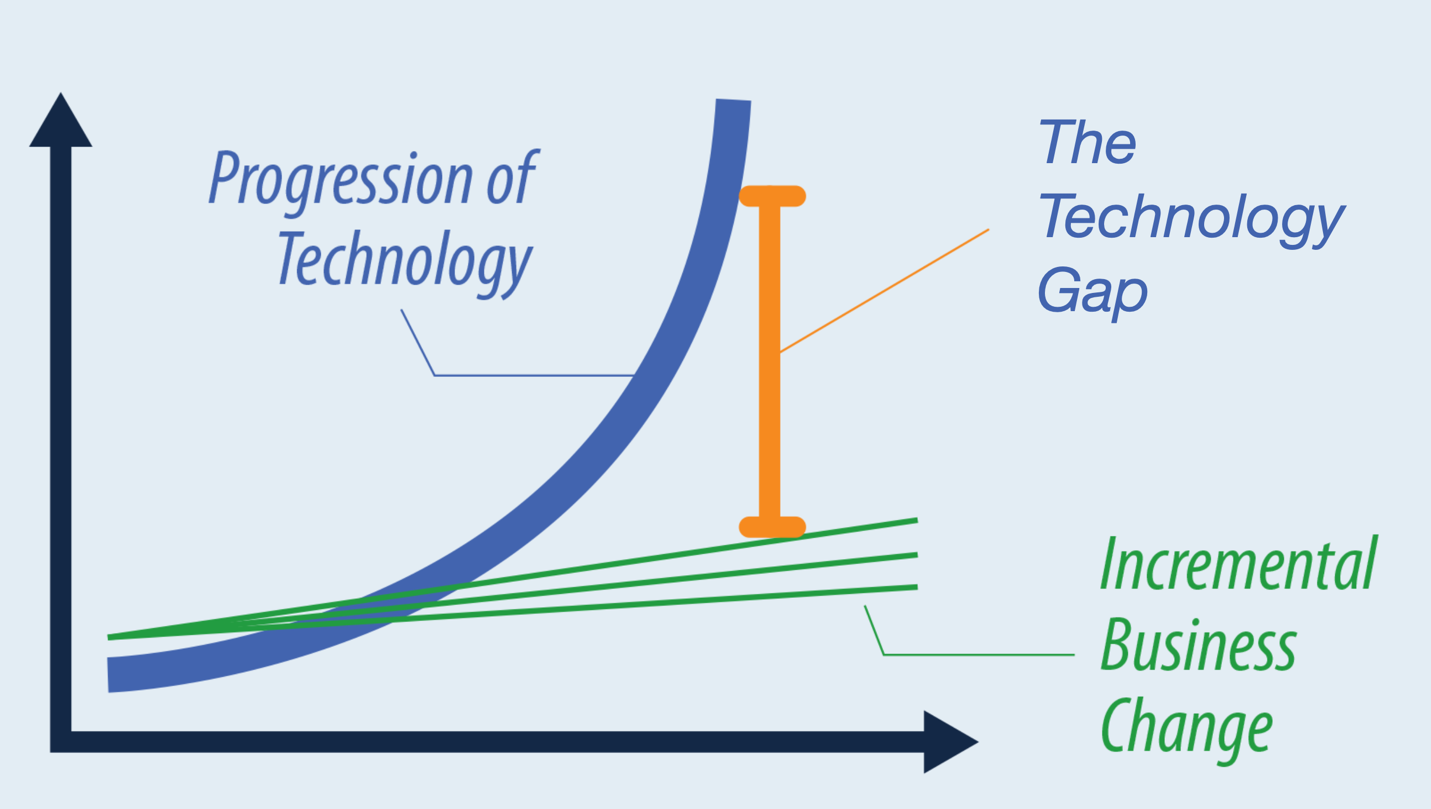

As a result, as illustrated in Figure 1, the gap between what’s possible to do with technology and the incremental advance of best practice widens at an exponential rate. This ever-widening technology gap provides a rich basket of tools for insurers to pursue world-changing aspirations.

Figure 1: The Technology Gap

The list of powerful technology-enabled capabilities available, including the Internet of Things (including smart, embedded, mobile, flying and orbiting ones), artificial intelligence, big data, machine learning and predictive analytics, cloud and edge computing, blockchains, smart contracts and genomics, to name just a few.

A McKinsey study smartly synthesizes these capabilities into four trends that put insurance “on the verge of seismic, tech-driven shift.” The list provides a useful summary: explosion of data from connected devices; increased prevalence of physical robotics; open source and data ecosystems; and, advances in cognitive technologies.

These trends and the underlying technologies are already being deployed, as the McKinsey authors point out, and are sure to drive dramatic changes across the insurance value chain. Insurers must master them to get faster, better and cheaper in core functions that support their existing products, such as distribution, underwriting, pricing, claims and service. And, they must to do so faster than the competition, or risk falling behind even as they advance.

The bigger, world-changing opportunities lay in stretching beyond the incremental and also harnessing the technology gap for innovations that lessen the risk gap.

How do these trends translate into new opportunities to reduce the climate protection gap, such as by leveraging advances in high resolution global and regional climate modelling, weather and climate change simulation and forecasting capabilities and real-world data from space, ocean and terrestrial platforms?

How do AI-augmented models crunch big data to address other protection gaps, such as business interruption, contingent business interruption, supply chain fragility, manufacturing and production risk, economic demand surges (and plunges) and the impact of climate risk on financial modeling and investment risk analysis?

How do pervasive communications, smartphones and new edge devices allow for the reimagining of distribution, claims and service to serve the previously under and inequitably served, rather than just better serve existing customers?

These are but a few of the questions worth asking about how the underleveraged tools in your organization’s Technology Gap be applied to address the Risk Protection Gap.

* * *

It would be easy to throw up one’s hands in the face of the massive gaps in risk protection and just focus instead on seemingly more tractable daily, weekly and quarterly concerns. It would be easy to leave world-changing aspirations to other, bigger global concerns to address, such as the United Nations, national governments and their policy makers, billionaire philanthropists and non-profit, non-governmental organizations.

Clearly, much remains to be done at the very macro levels, including international agreements and national policies, laws and regulations. The insurance industry as a whole and many individual companies within the industry are sizeable enough to step into these discussions. Some have done so; many could do more.

Making our very risky world a better place, however, requires both global policy orchestration and thousands of points of bottom-up innovation to better understand, pool and redistribute risk. The insurance industry certainly has the wherewithal to contribute mightily to this collective, on-the-ground effort. What will your company do? What can you do?

In part 2 of this series, I offer 5 strategies for identifying world-changing innovation opportunities that deserve your attention and a framework for incorporating them into your innovation portfolio.

11.2020

About the Author:

Chunka Mui is a futurist and innovation advisor who helps organizations design and stress test innovation strategies. He is the best-selling author of four books on strategy and innovation including The New Killer Apps: How Large Companies Can Out-Innovate Start-Ups and Billion Dollar Lessons: What You Can Learn From the Most Inexcusable Business Failures of the Last 25 Years. Chunka is also a regular contributor to Forbes. Chunka was previously managing partner and chief innovation officer of Diamond Management and Technology Consultants (now part of PWC) and co-founder and director of Vanguard. Chunka holds a B.S. in computer science and engineering from MIT.