The Forgotten: Understanding and Navigating the Generation X Retirement Gap in the United States

![]()

![]()

Maggie Carter, Head of Internal Audit, Equitable![]()

![]()

![]()

Executive Summary

Generation X, also known as “the forgotten generation”, in the United States is approaching retirement with less confidence than other generations and a sizable retirement gap. This group includes c.65 million Americans between the ages of 45 – 60 and is the next generation set to retire behind the Baby Boomers. This group has not received as much marketing or media attention to date as the Boomers who preceded them or the Millennials who follow them. Meanwhile, their working years have been filled with uncertainty as they endured through a changing retirement landscape, several significant economic events, and some unique challenges such as supporting children and aging parents simultaneously. Also, with inflation, rising healthcare costs, and social security uncertainty they are likely to encounter additional challenges during retirement. However, it is not too late for this generation to narrow their retirement gap. Many of these individuals are at the peak or approaching the peak earning years of their careers, which means they still have time and resources to boost their retirement savings. The time to focus on this generation is now and our industry can help. Some key elements of help should include education on financial planning and retirement, access to digital tools and retirement income solutions, and building confidence and trust. Innovative solutions tailored to address the unique challenges and preferences of this group will be needed to inspire action.

Introduction

This paper explores the retirement gap of Generation X in the United States and the role the insurance industry can play in helping this generation to increase their retirement readiness. The retirement gap represents the difference between the amount of retirement savings and the amount needed to support desired income in retirement. This paper considers experiences which have shaped the characteristics and behaviors of this generation and the resulting influence on their preparation and outlook toward retirement. It also explains why the time is now to focus on this generation and covers some actions which can be taken to help these individuals have more financial security in retirement.

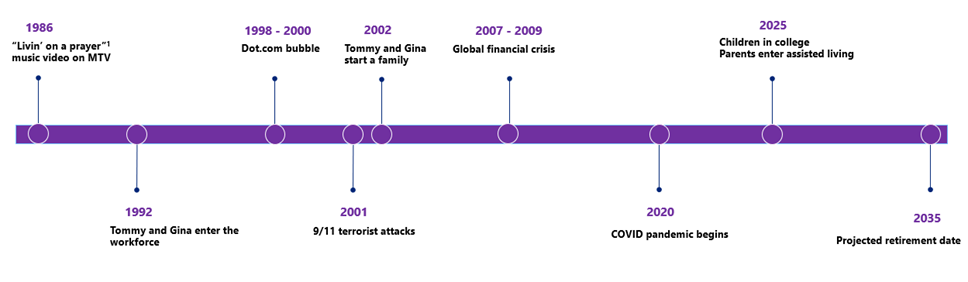

To put this problem into context, let me begin by introducing you to Tommy and Gina, a Gen X couple about 10 years from retirement. They grew up during the rise of MTV with the media and cultural influence of the times shaping their attitudes and perspective. Tommy and Gina met in college and entered the workforce after their graduation in 1992. This was a challenging time to enter the workforce as the job market growth was slow following an economic recession in 1990-1991. However, it was also a period of technology growth with desktop computers and the internet emerging, thus fundamentally changing the way people worked. Furthermore, the responsibility for retirement planning was shifting to employees with many employers moving away from defined benefit pension arrangements and moving toward defined contribution plan offerings such as 401k accounts. This meant that in addition to covering daily living expenses and repaying their college debt, Tommy and Gina had to start individually saving and investing for their future retirement. Thus, the early part of their careers was marked by change, uncertainty, and challenge. Nevertheless, they managed to start their careers and invest in their future by contributing to a 401k. Their 401k contribution rates started at a low percentage as they needed most their paychecks to cover living expenses in the early years, but over time their contributions grew.

Throughout their working years, there were several events which led to economic disruptions, such as the dot.com bubble, the terrorist attacks of 9/11, the global financial crisis, and the COVID pandemic. These events caused economic setbacks and uncertainty which Tommy and Gina had to overcome, causing some fluctuations in their retirement savings patterns. Today Tommy and Gina are in the peak years of their careers, but a new set of challenges has emerged with shifting family dynamics as their children are in college or recently graduated and their aging parents need an increasing amount of care. By the time they reach retirement in 2035, the U.S. social security trust account may be depleted resulting in a potential reduction in social security benefits for retirees. Accordingly, they will need more individual retirement savings to supplement social security payments and secure their income needs in retirement. With 10 years to go until retirement and the added financial strain of currently paying high college tuition expenses while supporting their parents’ assisted living needs, Tommy and Gina are not sure how they will boost their savings to make up the projected shortfall in retirement income. However, they recognize the need to find a solution rather than “Livin’ on a Prayer”1.

Tommy and Gina’s journey:

![]()

Background:

Who is this generation?

Generation X in the United States includes c. 65 million individuals born between 1965 – 1980. This generation entered the workforce in mid 1980s through the 1990s and the first of them are turning 60 this year, making Gen X the next generation to approach retirement. They have less confidence in their retirement savings than other generations with 54% concerned or very concerned that they will outlive their assets according to a Schroders survey2. The average gap between anticipated retirement savings and the amount Gen Xers believe they will need to retire comfortably exceeds $460,000, which is larger than the anticipated shortfall for individuals in other generations2. This generation is known for their self-reliance and independence, embraces technology, and has shown resilience to uncertainty and change. They also tend to have a certain amount of skepticism, perhaps driven by media, music, and movie influences of their times.

Table 1 Retirement Gap by Generation

Baby Boomers | Gen X | Millennials | |

Birth Years | 1946 - 1964 | 1965 - 1980 | 1981 - 1996 |

Retirement Gap2 | $353,069 | $466,802 | $322,128 |

What influences have shaped their views and behavior?

Generation X came of age during a time of significant change, both social and economic, which influenced their behaviors, preferences, and financial outlook. Understanding these drivers is fundamental to determining solutions and the approach which may resonate with Gen X pre-retirees.

- Family life and social influences: Gen X has also been referred to as the “latchkey kids”, a term which refers to their typical upbringing in households with two working parents or single parents which meant the children had to become more independent at an earlier age. This resulted in a generation of individuals which is known for their self-reliance. That self-reliance can be seen in some of their preferences for advice and financial products, such as utilization of online investing, which is important to understand when designing solutions to fit the needs of this generation. From a social standpoint, they grew up during the rise of MTV and other media influences giving them access to more information, both good and bad. This information, and the manner in which it was shared, shaped this generation’s cultural awareness, preferences for consuming information, and even certain attitudes such as their independence mindset.

- Technology advances: Change has been a constant for this generation and that included the technological advances throughout their childhood and working years. This generation saw the rise of personal computers, the internet, and mobile devices to name a few. Thus, they are adept at embracing and adapting to new technology solutions. Situated with a unique perspective of observing both the pre and post digital era, this generation can see the value in both and take a balanced approach when adopting new technology.

- Shift in retirement savings landscape: Gen X is the first generation to become predominately reliant on defined contribution plans as a method of saving for retirement as many employers were shifting away from defined benefit pensions as this group entered the workforce. According to research from the Insured Retirement Institute (IRI), only 23% of Gen Xers surveyed expect income from a private pension during retirement3. The shift to defined contribution plans shifted more of the savings responsibility and risk to the employees as these plans required more self-directed choice, such as contribution levels and investment elections. In the early years of defined contribution plans, certain features such as auto-enrollments were not as common, which may have impacted the savings rates for Generation X in the financially critical first stages of their careers.

- Notable Economic Events: Several notable events throughout their lives, and in particular working years, have shaped this generation’s perspectives and financial outlooks. Many entered the workforce in time to see the dot.com bubble burst which was shortly followed by the terrorist attacks of 9/11 which had profound impacts on the US workforce and economic environment. Next, a global financial crisis hit in 2008 leading to market loss and unemployment, which was an important time in this generation’s careers, a time of foundation building for their financial security. Then, after a period of rebuilding and career growth following the financial crisis, the COVID pandemic emerged in 2020 which introduced a new set of challenges. Considering the uncertainty driven by these events, some of which occurred at formative times in their careers, it is not surprising this group is less confident about retirement than other generations with only 54% of survey respondents indicating they are on track for a financially secure retirement4.

What challenges will impact their retirement readiness?

Generation X is facing many challenges as they approach retirement, some of which may continue into their retirement years impacting how far their savings will go and how long it will last. According to a 2024 US retirement survey, only 14% of Gen X respondents believe they have sufficient retirement savings2. A key element underpinning their retirement readiness is insufficient planning, exacerbating the risks associated with other challenges which lie ahead for this group. Without proper planning, Gen Xers may find it more difficult to overcome challenges which may diminish the sufficiency of their savings and thus impact their ability to live comfortably during retirement.

- Lack of financial planning: Only 27% of Gen Xers surveyed are working with a financial advisor and 48% have not done any retirement planning, according to a Schroders survey2. Without proper planning, individuals in this generation may be missing critical steps to ensure they reach retirement with enough savings to live comfortably through its duration.

- Sandwich generation: Gen X is often referred to as the “sandwich generation” due to the combined strain of caring for their children and aging parents at the same time. Many individuals in Gen X have children currently in college with high tuition expenses or early career children who are still relying on their financial assistance due to startup expenses associated with independent living. At the same time, many of these Gen Xers are caring for their own parents who need increasing levels of care or even financial support for professional assisted living care. This financial strain may place extra pressure on this generation’s ability to save more and catch up on their retirement goals.

- Longevity: With individuals living longer, retirement savings will need to last for a longer period as individuals may spend more years in retirement than prior generations. This is a concern for Gen X as this group has low confidence in their savings lasting for a longer period, with only 32% indicating confidence that their retirement savings will last until age 853. Overall, Gen X appears to have a greater fear of outliving their savings than other generations, with 72% of survey respondents fearing running out of money more than death5.

- Inflation: Inflation is a key challenge for retirement planning as rising expenses can impact the amount of money individuals are able to set aside for retirement savings. Although the current inflation rate is down from its recent surge in 2022, many Gen Xers express concerns with this challenge. According to a 2023 Natixis global investor survey, 55% of Gen Xers report saving less due to higher expenses6. Furthermore, inflation is one of those challenges that will also continue to impact individuals during the retirement years as a retiree’s real income may not be enough to cover rising expenses. A survey conducted for the Society of Actuaries (SOA) Research Institute found that 63% of Gen Xers are concerned that the value of their savings might not keep pace with inflation4.

- Rising healthcare costs: Another concern impacting savings is rising healthcare costs. Almost 25% of Gen Xers indicate that going broke in their efforts to cover healthcare expenses is one of their greatest retirement fears6.

- Social Security uncertainty: With rising concerns around the sustainability of Social Security benefits in the United States beyond 2035, Gen X could be a generation directly impacted by a reduction in benefits and will need to plan for other sources of savings to live comfortably in retirement. When asked about concerns surrounding social security benefits, 62% of Gen Xers surveyed were extremely or very concerned about the availability of Social Security when they retire and 54% indicated that they were extremely or very concerned that it would not be enough to cover their expenses, according to a Corebridge longevity survey5. Furthermore, 43% of Gen Xers plan to take Social Security benefits before age 70 due to their concerns around the ability of Social Security to make future payments2.

- Debt: Gen X also carries higher debt than other generations, with high credit card debt, mortgages, and remaining student loan balances. Managing this debt can impact their ability to save for retirement. According to a survey by Allianz Life, 64% of Gen Xers surveyed are working to pay off debt to meet long term goals7.

Proposed Solutions:

What can the insurance industry do to help?

Financial planning and retirement education. While Gen Xers recognize the need for financial advice, many have not yet taken the steps to seek that advice and adequately prepare for retirement. According to a survey by Allianz Life only 35% of Gen X respondents have a financial professional7, and only 27% are working with a financial advisor according to the Schroder’s survey2, indicating the vast majority are not utilizing financial advice. This is where our industry can lean in and help these individuals. With targeted outreach to this generation, professionals in our industry can help Gen X with planning and education around solutions to help them meet their retirement goals.

- Financial planning: Assisting Gen Xers with the development of a retirement plan may help boost their confidence toward retirement and help increase their preparedness to address future retirement challenges. Financial advice from a professional can also help Gen Xers evaluate key decisions such as what age to take Social Security benefits, identifying options to generate additional retirement income, and prudent decumulation strategies to avoid outlining savings. Fifty-six percent of Gen Xers surveyed indicate they need professional advice, with financial planning and retirement income planning being two of the services they want6.

- Education: Education on options available to help Gen Xers boost their retirement savings as well as awareness of some of the challenges, such as inflation which may impact the purchasing power of their savings during retirement, can help Gen Xers as they execute on their retirement plans. For example, some individuals may be able to take advantage of 401k and IRA catch-up contributions, which are $7,500 and $1,000 respectively in 2025, to help boost their savings. Furthermore, many Gen Xers recognize the need for broader financial education and investment knowledge with 47% indicating a desire for their financial advisor to help them understand investing6. Also, insurance products offering tax-deferred growth or guaranteed income solutions may offer additional ways to boost savings or provide income security. However, the first step to action is making sure individuals are aware these options exist and that they understand the potential benefits and risks.

Access to personalized advice, digital tools, and retirement income solutions. Consistent with the ever-changing technology landscape in their lifetime, this generation is accustomed to change and embraces technology enabled solutions. They prefer a combination of self-directed options, given their self-reliant nature, and the expertise and connections offered in human advice. They also recognize the need for more saving and income solutions to help them meet their needs in retirement.

- Balanced Approach: In line with the balanced approach many Gen Xers take in adoption of new technologies, they can see the value of both digital solutions and the expertise and guidance associated with financial planning. Many Gen Xers prefer a combination of collaborative advice and self-directed technology solutions for their financial planning needs. According to a State Street Global Advisors study, over 50% of Gen Xers surveyed are self-directed investors lacking the tools and guidance they want, with 41% of these self-directed Gen Xers citing the lack of guidance as a shortcoming of self-service platforms8. Thus, the insurance industry should approach this group with a proper balance of hands-on, personalized advice and digital solutions.

- Income Solutions: Additionally, this generation is seeking income solutions to supplement their retirement savings. According to a Corebridge longevity survey, 73% of Gen X respondents would have more confidence about a comfortable retirement with a source of guaranteed monthly income to supplement social security5. Furthermore, 60% of Gen X respondents in an IRI survey indicated that income sources being guaranteed for life was very important with another 23% ranking it at somewhat important3. That same IRI survey showed that Gen X indicated a preference for risk management solutions and lifetime income options within defined contribution plans3. This is one way in which the insurance industry can help through products which offer access to guaranteed income, such as annuities or in-plan guarantees. However, education and marketing outreach to this group will be needed to inspire action as only 17% of Gen Xers surveyed by IRI indicated that they planned to purchase an annuity3.

Establish and maintain trust in our industry. While Gen X values personalized advice and interactions, trust is a key requirement for their advisor relationships. This generation is often known for their cynicism with only 48% of Gen Xer’s surveyed indicating that they trust financial media when making decisions6. Thus, in order to effectively reach this market, the industry will need to gain and maintain the confidence of these investors.

- Skepticism: The cynical nature of Gen X results in a skeptical outlook toward some institutions and authority. It may have resulted from the family and societal factors which shaped their upbringing, such parental styles which fostered a do-it-yourself attitude and the uncertainty with economic events.

- Transparency: To overcome this perception, the industry will need to exhibit transparency and personalized solutions exhibiting an understanding of their unique situation. This may include providing clear explanations of the basis for projections or solutions. Also, avoiding the use of jargon will help by reducing complexity and enable a more straightforward communication style which is preferred by Gen X. They also place importance on evidence with a ”see it to believe it” mindset. Thus, evidence-based, practical examples may resonate with this group when making financial decisions.

Why now?

This generation still has time to save and grow their retirement assets as some individuals are still 10 – 20 years from retirement, and there are solutions available to help them save such as tax-deferred retirement plans and catch-up contributions for individuals over the age of 50. However, time is limited, and many have not done any planning. Many individuals in Gen X are in or approaching the peak earning years of their careers, which is a key factor that could enable them to start boosting savings, so long as the other challenges mentioned above can be managed. According to Vanguard’s How America Saves 2025 report, only 16% of eligible participants over age 50 utilized catch-up contributions in 20249. Gen Xers are holding 35% of their retirement assets in cash on average, with 64% of those surveyed citing fears of market downturns as a reason2. Generation X currently has the 2nd highest total assets among generations in the United States, behind the Baby Boomers who hold the most, according to the UBS Global Wealth Report 202510. Also, Gen X is set to inherit a sizable amount in the next decade as part of the anticipated “Great Wealth Transfer” from older generations, with Cerulli estimating nearly $1.4 trillion, on average, annually going to Gen X11. This generation should be a key audience for the solutions offered by our industry. They need income solutions, financial planning, and advice now to help grow and manage their assets and navigate their remaining road to retirement.

Conclusion:

Even though Gen X is facing a sizable retirement gap along with many current and future challenges ahead as they navigate to and through their retirement journey, there is still time to act, and that time is now. I started this paper by walking you through Tommy and Gina’s journey, explaining how influences, challenges, and events in the world around them have shaped their perspectives and path to retirement. Tommy and Gina are only one example though. This generation is 65 million individuals large in the U.S., and many of them face similar challenges to Tommy and Gina. As an insurance industry, we can help them navigate their retirement journey through planning assistance, education, and product offerings such as income solutions to help them bridge the current gap. They value professional expertise and advice, but solutions need to be balanced with the convenience and independence offered by self-directed digital solutions. Now that we understand the factors which influenced and shaped this generation and the challenges they face, we need to use that information to figure out how best to engage with Gen X to inspire action. Innovative solutions, either in product design or marketing outreach, should be tailored to address the challenges and unique preferences of this generation. Also, timing will be critical, intervening at the right time and making the conversation relevant to their individual priorities will be key to getting their attention. Through a backdrop of constant change, Generation X has persevered to navigate through their careers and reach the pre-retirement years. As they enter this next phase of their journey, nearing retirement, let’s refocus our attention to make them an ‘unforgotten’ generation and help them to retire with certainty and security.

References

- “Livin’ on a Prayer” – written and recorded by Jon Bon Jovi, Richie Sambora and Desmond Child, 1986.

- “The lost-retirement generation”, Schroders 2024 US Retirement Survey: Generation X and retirement report, Schroders, 2024, https://www.schroders.com/en-us/us/institutional/clients/defined-contribution/schroders-us-retirement-survey/generation-x-and-retirement/.

- “July 2023 IRI Research Brief: Evolving Retirement Expectations Among American Workers and Retirees”, Insured Retirement Institute, July 2023, https://www.irionline.org/wp-content/uploads/2023/07/IRI-Research-Brief-2023.pdf.

- “Generation X: Ready for Retirement?”, SOA Research Institute, February 2022, https://www.soa.org/49153e/globalassets/assets/files/resources/research-report/2022/2022-gen-x-retirement.pdf.

- “Don’t you forget about me: Getting the MTV generation (Gen X) successfully to and through retirement”, Corebridge Financial Survey on Longevity; Corebridge Financial, 2023, https://www.corebridgefinancial.com/insights-education/genx.

- “Generation X Report: Reality Bites, Retirement anxieties grow as Generation X turns 60”, Natixis Investment Managers, 17 June 2024, https://www.im.natixis.com/en-us/insights/investor-sentiment/2024/gen-x-report.

- “Gen X Approaching Retirement Crunch Time with Savings Regrets”, Allianz Life, 2024 Annual Retirement Study, Allianz Life, 13 June 2024, https://www.allianzlife.com/about/newsroom/2024-Press-Releases/Gen-X-Approaching-Retirement-Crunch-Time-with-Savings-Regrets.

- “State Street Global Advisors Study: Advisors Capture Four Influential Investor Segments With A Combination of Old Fashioned Collaboration and Modern Technology”, State Street, 03 June 2024, https://investors.statestreet.com/investor-news-events/press-releases/news-details/2024/State-Street-Global-Advisors-Study-Advisors-Capture-Four-Influential-Investor-Segments-With-A-Combination-of-Old-Fashioned-Collaboration-and-Modern-Technology/default.aspx.

- “How America Saves 2025: Data that Leads”, Vanguard, June 2025, https://institutional.vanguard.com/insights-and-research/report/how-america-saves-2025.html.

- “Global Wealth Report 2025: Crafted wealth intelligence”, UBS, 2025, https://www.ubs.com/us/en/wealth-management/insights/global-wealth-report.html.

- “Generation X Represents the Most Immediate Opportunity for Wealth Managers”, Cerulli Associates, 30 June 2025, https://www.cerulli.com/press-releases/generation-x-represents-the-most-immediate-opportunity-for-wealth-managers.